The Euro, the Dollar, the Yuan. The Credit rating

Agencies. A complex game of global chess in which a click of the mouse

can affect the pricing of a country's Sovereign Bonds overnight. Let us

take a look at the current (29/11/2012) S&P ratings of some of the

largest EU economies. These obviously have an immediate and immense

effect on bond pricing.

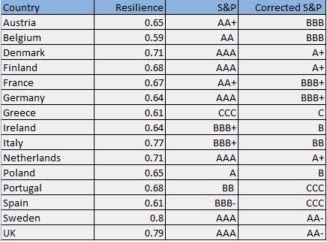

The above table indicates, for example, that there are 5 AAA economies in the troubled Eurozone. This is clearly a contradiction. When the entire continent is in a state of extreme fragility (see our blogs on the subject - the EU has a very low 50% resilience since late 2010!) and when there are questions as to the survival of the EU, one asks: can there be AAA economies in such a situation? Clearly not. In a global planetary economy meltdown there are no AAA countries. The objective of this blog, is, in fact, to reveal how very distorted the information in the above table is.

The above table indicates, for example, that there are 5 AAA economies in the troubled Eurozone. This is clearly a contradiction. When the entire continent is in a state of extreme fragility (see our blogs on the subject - the EU has a very low 50% resilience since late 2010!) and when there are questions as to the survival of the EU, one asks: can there be AAA economies in such a situation? Clearly not. In a global planetary economy meltdown there are no AAA countries. The objective of this blog, is, in fact, to reveal how very distorted the information in the above table is.

Conventional ratings don't take into account resilience - the fundamental property of a system which makes it able to survive shocks. Today, the economy is governed by turbulence and shocks and one would expect analysts to take resilience into account. Imagine a doctor treating a patient for obesity without considering cholesterol. The table below lists the resilience for each economy indicated above.

A resilience of 1 indicates a highly resilient situation, values close to 0 point to extreme fragility. It is clear that in term of pure resilience things look a bit different. Italy, for example, a G7 economy, has been under constant attack by the Rating Agencies while it has an economy that is significantly more resilient and prepared to sustain shocks (e.g. Eurozone breakup) than Germany. Germany is very much dependent on exports, its banking system is in a worse condition than those of Italy. Italy's banks have very low foreign exposure, see graph below.

The exposure of German, French and the UK banks is very high, Italy's is not even comparable. While we don't deny that Italy too has its troubles, what is not clear is why the above mentioned countries enjoy AAA status. Moreover, Italy has EU's second manufacturing industry, second only to Germany, but, as consequence of the series of speculative attacks and downgradings, it is forced to offer its bonds at substantially higher rates than logic would suggest. Recently, Italy's Central Bank has claimed that these downgrades and attacks are costing the country approximately 200 base points. This is a huge amount. In other words, Italy is paying 2% more interest on its bonds than it should.

We have recently performed an original experiment, in which we have corrected S&P ratings using resilience. Without going ino the analytical details of the procedure, here are the new "corrected" ratings.

The spread between the various economies has been reduced substantially and reflects more realistically the current situation which, however, downgrades almost every country by at least a couple of notches. This is much more in line with the overall resilience rating of the Eurozone which, at 50%, indicates extreme fragility. Maybe investors should start asking questions..... more soon.

No comments:

Post a Comment