(written in 2005)

Every dynamical system possesses a characteristic

value of complexity which reflects how information is organized and how

it flows within its structure. Like most things in life, complexity is

limited. In fact, there is an upper bound on complexity that a given

system may attain and sustain with a given structure. This

‘physiological’ limit is known as critical complexity. In the proximity

of its corresponding critical complexity every system becomes fragile

and therefore vulnerable. This fragility is consequence of a very simple

fact: critically complex systems possess a multitude of modes of

behaviour and can suddenly jump from one mode to another. Very often,

minute amounts of energy are sufficient to accomplish such mode

transitions. Consequently, highly complex systems may easily develop

surprising behaviour and are inherently difficult to understand and

govern. For this very reason, humans prefer to stay away from situations

that are perceived to be highly complex. In the vicinity of critical

complexity, life becomes more risky precisely because of the inherent

element of surprise.

In the past few years modern complexity science has developed

comprehensive metrics and means of measuring not only the complexity of

generic systems but also the corresponding critical complexity. This has

enabled to turn the above intuitive rules into rational general

principles which govern the dynamics and interplay of everything that

surrounds us. The interaction of entropy and structure is the

fundamental mechanism behind co-evolution and behind the creation of

organized complexity in Nature. Higher complexity implies greater

functionality and therefore higher ‘fitness’. However, extreme

specialization – fruit of ‘evolutionary opportunism’ – comes at a high

cost. Robust yet fragile is the hallmark of highly complex systems.

Think of how creative the human species is and yet how fragile human

nature is. Under highly uncertain and stressful conditions this

fragility emerges with strength. But since human beings are the basic

building blocks of societies, economies and nations, it is not difficult

to understand why the complexity of our globalized and turbulent world

assumes almost cosmological proportions. Fragility and volatility are

words which best reflect the state of health of not only the global

economy but also of the society in all of its aspects.

Our global society is ultimately a huge and dynamic network, composed of

nodes and links. The connections between the nodes (individuals,

corporations, markets, nations) are rapidly increasing in number, just

as is the number of nodes. A fundamental feature of this network is

entropy, which is a measure of uncertainty. Because the nodes do not

always act in a rational and predictable fashion, the connections are

“noisy”. Because the amount of entropy can only increase – this is due

to the Second Law of Thermodynamics - while new connections are being

created every day, many others are destroyed. This process is also

inevitable. The measure of complexity is a blend of the topology of the

network and the amount of noise – entropy – contained within its

structure. Consequently, there are two means of increasing complexity:

adding more structure (connections, nodes or both), or, for a given

network structure, increase the amount of noise.

In the past, the Earth was populated by numerous and disjoint

civilizations that thrived almost in isolation. The Sumers, the Incas,

or the Romans are just a few prominent examples. Because the temporal

and spatial correlation between those civilizations was very limited, if

one happened to disappear, many more remained. However, the Earth today

is populated by one single globalized society. If this one fails,

that’s it. But any form of progress is accompanied by an inevitable

increase in complexity. This is true only until critical complexity is

reached. In order to continue evolving beyond critical complexity, a

civilization must find ways of overcoming the delicate phase of

vulnerability in which self-inflicted destruction is the most probable

form of demise.

When a society approaches critical complexity, it has the following alternatives in order to survive:

1. Reduce its complexity. This is done by dumping entropy or by simplifying its structure. In practice this translates to:

- Stricter laws.

- Less laws.

- Reduction of personal freedom.

2. Learn to live in proximity of critical complexity. This is risky because the system is:

- Extremely turbulent (stochastic). Terrorism, crime and fraudulent behaviour thrive close to criticality.

- Very difficult to govern – impossible to reach goals.

- Unexpected behaviour may emerge.

- On the verge of widespread violence.

3. Increase its critical complexity. This may be accomplished in essentially two ways:

- Creating more links (making a denser Process Map). However, this makes governing even more difficult.

- Adding structure. Certainly the preferred option. One example?

“Create” more nations – this not only increases structure, it may also

help ease tensions.

Option 2 is the most risky. Living in proximity of

critical complexity cannot be accomplished in the framework of a

conventional western-type democracy. The extreme turbulence which

characterizes critically complex systems is most likely better dealt

with in a technocratic and police-state setting, which limits severely

personal freedom. Only a government which understands how to actively

manage complexity on a vast scale may venture into similar territory. To

our knowledge, solution 2 is today not viable. A better approach,

therefore, is to adopt a mix of 1 and 3.

Terrorism constitutes surely one of the major concerns of modern

democracies. The number of terrorist attacks has more than tripled in

recent years. Contrary to popular belief, religion is not the main

motivating factor. In terms of location most instances of

politically-fuelled violence and terrorism may be found in Asia, not in

the Middle East. In fact, our research shows that Asia enjoys a far

greater complexity growth rate than the Middle East. Approximately one

fourth of trans-national politically-motivated terrorist acts are

inspired by religion. A similar amount is accounted for by leftist

militant organizations. Nearly 40% of terror acts are perpetrated by

nationalist and separatist groups. As expected, there is no single clear

cause. A mix of factors, which ultimately lead to some form of social

injustice, poverty, failing states or dysfunctional politics are what

fuels terrorism. This suggests that the problem is indeed due to very

high complexity. We are also painfully aware of the fact that modern

democracies naturally lack efficient tools to effectively deal with

highly complex socio-political-ethnical and religious problems, without

neglecting the fundamental economical and ecological dimensions.

Where can terrorism develop with greater ease? Terrorists need to hide.

For this reason they thrive in high-entropy environments, such as

failing or rogue states, where there is little social structure. It is

in highly complex societies (doesn’t mean developed) that terror groups

find geo-political sanctuaries. High complexity, as mentioned, comes in

many forms:

- Little structure but high entropy (Third World countries)

- Much structure, low entropy (Western democracies)

- Much structure, high entropy (the future global society)

Terror groups generally prefer high entropy-dominated complexity because

of the Principle of Incompatibility: high complexity implies low

precision. This means that hunting them down - essentially an

intelligence-driven exercise - is difficult because of lack of precise

information, laws on privacy, etc. Because of the fact that globally

complexity is quickly increasing, it will be increasingly more difficult

to identify terror groups especially in ambiguous countries, i.e. those

which harbour terrorists but are willing to close an eye. The problem

with Western countries is that they are becoming more permissive and

tolerant, leading to an overall erosion of social structure in favour of

entropy. In underdeveloped countries it is almost impossible to create

new social structure hence it is entropy that causes the increase of

complexity. In the West, the more intricate social structure is being

eroded by loss of moral values and relativism. The result? in both cases

an increase in complexity. Following the above logic, we can state

that:

- High complexity is necessary (but not sufficient) to lead to terrorism.

- Terrorism in an almost “obvious” consequence of a highly complex world.

- The Principle of Incompatibility and terrorism are intimately linked.

Can complexity be used to anticipate conflicts, crises and failing

states? The answer is affirmative. It is evident that a society/country

in the proximity of its critical complexity is far more open to enter a

state of conflict, such as civil war or simply declare war on a

neighbouring country. The conditions that a society must satisfy in

order to switch to a conflict mode are multiple. As history teaches,

there is no established pattern. Many factors concur. But it is clear

that it is more difficult to take a well functioning and prosperous

society to war than one which is fragile and dominated by entropy. In a

society in which the entropy-saturated structure is eroded, the distance

that separates a “peace mode” from a “conflict mode” is much smaller

and switching is considerably easier. The idea, therefore, is to measure

and track complexity region per region, country per country, and to

keep an eye on those countries and regions where high complexity

gradients are observed. Regions where complexity increases quickly are

certainly candidates for social unrest or armed conflict. How can this

be accomplished? What kind of data should be used? Good candidates are:

• Birth-rate

• Death-rate

• Debt-external

• Electricity-consumption

• Electricity-production

• Exports

• GDP

• GDP-per capita

• GDP-real growth

• Highways

• Imports

• Infant Mortality

• Inflation rate

• Internet users

• Labour force

• Life expectancy

• Military expenses

• Oil-consumption

• Oil-production

• Population

• Telephones mobiles

• Telephones-main lines

• Total fertility rate

• Unemployment rate

The list is of course incomplete, as there are tens of other indicators

which must be taken into account. Based on historical data such as that

listed above, Ontonix has conducted comprehensive analyses of the

World’s complexity and its rate of growth. It has emerged that if the

current trend is maintained, our global society shall reach criticality

around 2045-2050. What does this mean? The high amount of complexity

will make it extremely difficult to govern societies or to make

decisions of political nature. Under similar conditions, self-inflicted

extinction will be highly likely. Although from a global perspective,

the World is still almost half a century away from its critical state,

there are numerous regions of the World in which societies are nearly

critical and extremely difficult to grow and govern. Many parts of

Africa, the Middle East or South East Asia are just a few examples. But

also Western democracies are in danger. Highly sophisticated and

peaceful societies too are increasingly fragile because of a rapid

increase of rights, freedom, tolerance or relativism.

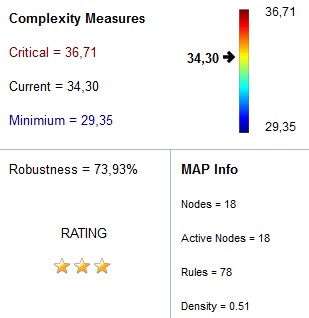

It is interesting to note how the global robustness

of the world has dropped from 77% in 2003, to 68% in 2004. Similarly,

in the same period complexity has increased from 6.3 to 8.1, while the

corresponding critical complexity has risen from 8.1 to 9.6. Critical

complexity increases because globally speaking the world’s economy is

growing. This is of course positive. However, this growth is lower than

the growth of complexity. The two values will cross around 2045-2050.

All ancient civilizations have collapsed. This is because due to a

variety of reasons they reached their critical complexity and were

unable to cope with the resulting fragility. Critical complexity becomes

a severe liability for a species especially once it acquires powers

more than sufficient for its self-destruction. Fragile civilizations are

vulnerable and their most likely fate

If we fail to cope with and, ultimately, move safely past criticality,

there will be no second chance, no other civilization will take over.

Clearly, the biological lifetime of our species is likely to be several

million years, even if we do our worst, but as far as technological and

social progress is concerned, that will essentially be it. Globalization

of course accelerates the increase of complexity until criticality is

reached. Critical complexity, on the other hand, is the hurdle that

prevents evolution beyond self-inflicted extinction. Since none of the

ancient (and not so ancient) civilizations have ever evolved beyond

critical complexity - in fact, they’re all gone - they were all

pre-critical civilizations. There has never been a post-critical

civilization on Earth. The only one left that has a chance of becoming a

post-critical one is of course ours. But what conditions must a

civilization meet in order to transition beyond criticality? Essentially

two. First, it must lay its hands on technology to actively manage

complexity. Second, it must have enough time to employ it on a vast and

global scale. Complexity management technology has been introduced by

Ontonix in 2005. This leaves us with about 40-45 years.

{kind=link}

{kind=link}