IBM has recently announced a new "way to program computers" - the so-called "cognitive computing" - see here - which uses "visual analytics" techniques to process (and display) data.

The method of "Visual Analytics" has been pioneered by Ontonix over a decade ago when we introduced and patented (in 2005) our model-free technique of data processing which actually mimics the human brain. The method doesn't use conventional mathematics or math models - it just "sees data" and extracts workable conclusions and knowledge from it. As data gets richer the system "learns" and accumulates the new information in the form of experience and rules. See our recent blog on "Computing Knowledge" here, where we speak of extracting "Cognitive Maps" from raw data. More on the subject can be found in this other recent article. On model-free methods read here.

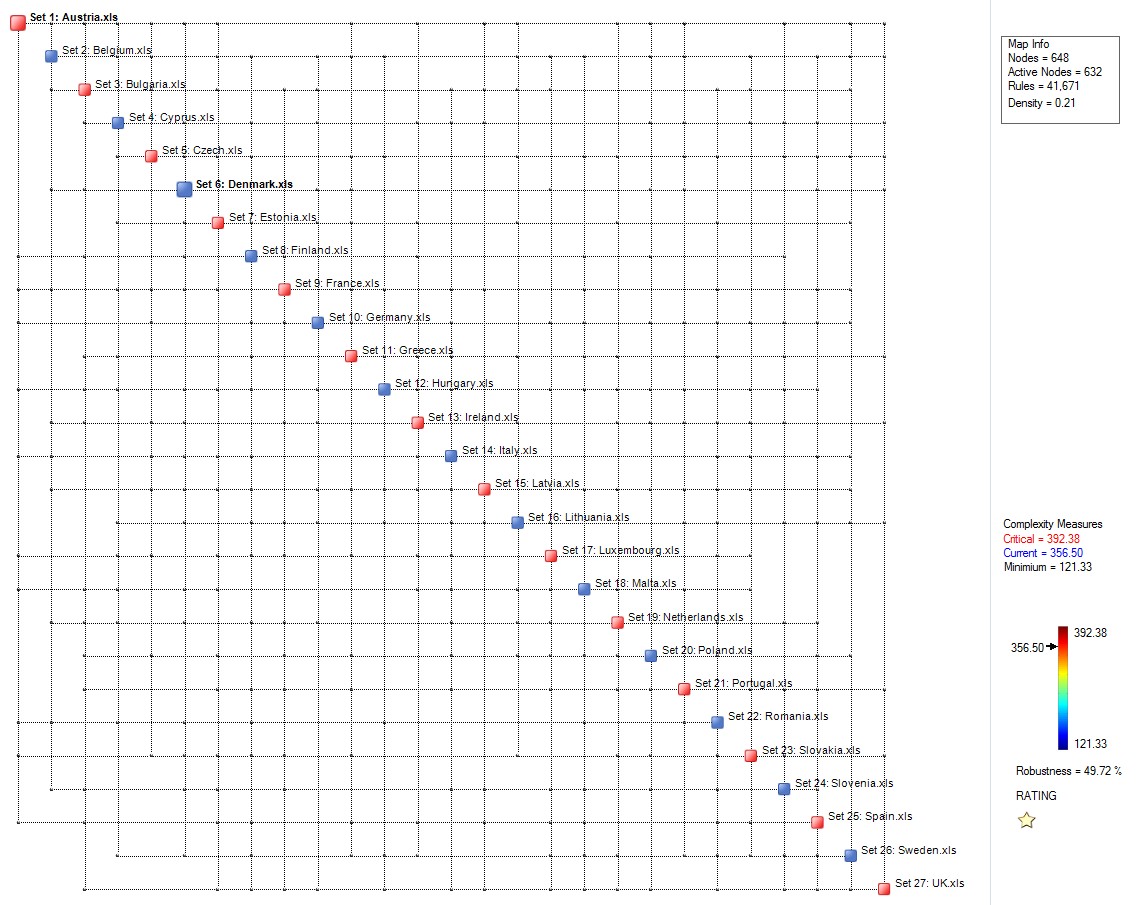

But there is more. We also measure the complexity of data as well as that of the resulting Cognitive Maps and, consequently, of the knowledge they contain. Knowledge and complexity are inextricably linked because complexity - which is measured in bits - actually quantifies the amount of structured information contained within a piece of data. But structured information is knowledge. More soon.

www.ontonix.com

{kind=link}

{kind=link}