Quantitative Complexity Management blog. Copyright (C) 2005-2013 Ontonix www.ontonix.com

Monday 23 September 2013

Ontonix S.r.l.: Is Risk Management a Source of Risk

Ontonix S.r.l.: Is Risk Management a Source of Risk: The deployment of risk management within a business can be a source of false assurance. Over recent years, businesses have becom...

Is Risk Management a Source of Risk

The deployment of risk management within a business can be a source of false assurance.

Over recent years, businesses have become more and more reliant on increasingly complex modelling processes to predict outcomes, to the point that in many cases, businesses have lost sight of what risk management is all about - and at the same time, risk management lost sight of what the business was all about. Increasingly, I have seen risk management services being deployed in large institutions by the 'big four' consultancy firms, and to keep their huge costs down, they end up with the newly qualified consultants - mid twenties, bright young things, but I'm sorry, they often don't have the faintest idea what your business does. They have insufficient real world experience to permit effective dissemination of risk knowledge.

I worked with one lovely young lady recently in a banking environment. Very intelligent - but she did not have the first clue of what the business was about. She made assumptions, and those assumptions lead the business down some long, dark alleys.

If you have risk function, however, that fully understands the business model, the deployment of its operational strategy, the sector the business operates in and the macro-economic and socio-political environment in which it operates, then they will be able to provide risk information that is relevant to the business, and can be understood by the business.

My hope going into this recession was that businesses would learn from this period in time, and take a more realistic, holistic view of the world. Worryingly, what I see is "more of the same".

I see financial institutions that have - on the face of it - bolstered their risk functions, but in doing so have allowed them to become ever more 'siloed' and fractured in their approach. This can only lead to disaster, in my view. The left hand will not know what the right hand is doing - no one owns anything, no one is responsible, no one is accountable.

So, I think the deployment of risk management has been a source of risk, but I don't think the dramas are over yet. There is a second wave of failure yet to hit, unless businesses can swallow the pill and take the right approach.

Over recent years, businesses have become more and more reliant on increasingly complex modelling processes to predict outcomes, to the point that in many cases, businesses have lost sight of what risk management is all about - and at the same time, risk management lost sight of what the business was all about. Increasingly, I have seen risk management services being deployed in large institutions by the 'big four' consultancy firms, and to keep their huge costs down, they end up with the newly qualified consultants - mid twenties, bright young things, but I'm sorry, they often don't have the faintest idea what your business does. They have insufficient real world experience to permit effective dissemination of risk knowledge.

I worked with one lovely young lady recently in a banking environment. Very intelligent - but she did not have the first clue of what the business was about. She made assumptions, and those assumptions lead the business down some long, dark alleys.

If you have risk function, however, that fully understands the business model, the deployment of its operational strategy, the sector the business operates in and the macro-economic and socio-political environment in which it operates, then they will be able to provide risk information that is relevant to the business, and can be understood by the business.

My hope going into this recession was that businesses would learn from this period in time, and take a more realistic, holistic view of the world. Worryingly, what I see is "more of the same".

I see financial institutions that have - on the face of it - bolstered their risk functions, but in doing so have allowed them to become ever more 'siloed' and fractured in their approach. This can only lead to disaster, in my view. The left hand will not know what the right hand is doing - no one owns anything, no one is responsible, no one is accountable.

So, I think the deployment of risk management has been a source of risk, but I don't think the dramas are over yet. There is a second wave of failure yet to hit, unless businesses can swallow the pill and take the right approach.

Posted by Andrew Bird, Managing Director at Nile Blue and freelance business consultant.

Saturday 21 September 2013

Ontonix S.r.l.: Measuring the magnitdue of a crisis

Ontonix S.r.l.: Measuring the magnitdue of a crisis: How can you measure the magnitude of an economic crisis? By the number of lost jobs, foreclosures, GDP drop, number of defaulti...

Measuring the magnitdue of a crisis

How can you measure the magnitude of an economic

crisis? By the number of lost jobs, foreclosures, GDP drop, number of

defaulting banks and corporations, deflation? Or by the drop in

stock-market indices? All these parameters do indeed reflect the

severity of a crisis. But how about a single holistic index which takes

them all into account? This index is complexity and in particular its

variation. Let us examine, for example, the US sub-prime crisis. The

complexity of the US housing market in the period 2004-2009 is

illustrated in the above plot. A total of fifty market-specific

parameters have been used to perform the analysis in addition to fifteen

macroeconomic indicators such as the ones mentioned above. The

"bursting bubble" manifests itself via a complexity increase from a

value of approximately 19 to around 32. With respect to the initial

value this means an increase of 40%. The arrow in the above plot

indicates this jump in complexity and this number represents a systemic measure of how profound the US housing market crisis is.

In summary, the magnitude of a crisis can be measured as follows:

M = | C_i - C_f | / C_i

where C_i is the value of complexity before the crisis and C_f the value during crisis. The intensity of a crisis can be measured as the rate of change of complexity.

Serious science starts when you begin to measure.

Friday 20 September 2013

Complexity: The Fifth Dimension

When complexity is defined as a function of

structure, entropy and granularity, examining its dynamics reveals its

fantastic depth and phenomenal properties. The process of complexity

computation materializes in a particular mapping of a state vector onto a

scalar. What is surprising is how a simple process can enshroud such an

astonishingly rich spectrum of features and characteristics. Complexity

does not possess the properties of an energy and yet it expresses the

"life potential" of a system in terms of the modes of behaviour it can

deploy. In a sense, complexity, the way we measure it, reflects the

amount of fitness of an autonomous dynamical system that operates

in a given Fitness Landscape. This statement by no means implies that

higher complexity leads to higher fitness. In fact, our research shows

the existence of an upper bound on the complexity a given system may

attain. We call this limit critical complexity. We know that in

proximity of this limit, the system in question becomes delicate and

fragile and operation close to this limit is dangerous. There surely

exists a "good value" of complexity - which corresponds to a fraction,

ß, of the upper limit - that maximizes fitness:

Cmax fitness = ß Ccritical

We don't know what the value of ß is for a given

system and we are not sure on how it may be computed. However, we think

that the fittest systems are able to operate around a good value of ß.

Fit systems can potentially deploy a sufficient variety of modes of

behaviour so as to respond better to a non-stationary environment

(ecosystem). The dimension of the modal space of a system ultimately

equates to its degree of adaptability. Close to critical

complexity the number of modes, as we observe, increases rapidly but, at

the same time, the probability of spontaneous (and unwanted) mode

transitions also increases quickly. This means the system can suddenly

undertake unexpected and potentially self-compromising actions (just

like adolescent humans).

Wednesday 18 September 2013

Stocks, Crowdrating and the Democratization of Ratings

{kind=link}

Assetdyne takes things forward even more. The company also provides a real-time rating system. Even though the system developed by Assetdyne focuses on publicly listed companies and portfolios of their stocks, it too introduces a fundamental new element into the process of rating - the so-called crowd-rating. The value of the stock of a company is the result of a complex interplay of millions of traders, analysts, investors, trading robots, etc. Ultimately, it is a reflection of the reputation and perceived value of a particular company and is the result of a democratic process. Clearly, the value of a stock is also driven by market trends, sector analyses, rumors, insider trading and other illicit practice and, evidently, by the Credit Rating Agencies themselves. However, undeniably, it is the millions of traders who ultimately drive the price and dynamics of stocks according to the basic principles of supply and demand. In practice, we're talking of a planet-wide democratic process of crowd-rating - it is the crowd of traders and investors that decides how much you pay for a particular stock.

What Assetdyne does is to use the information on the value and dynamics of the price of stocks to actually compute a rating. The rating that is computed does not reflect the Probability-of-Default (PoD) of a particular company - this the popular "AAA" kind of rating - it reflects the "resilience" of a given stock (hence the company behind it). Resilience is the capacity to resist shocks, a frequent phenomenon in our turbulent economy. Resilience, besides being a very useful measure of the state of health of any kind of system, not just of a corporation, possesses one very important characteristic - its computation is based on the measure of complexity. It so happens that complexity is the hallmark of our economy, of our times. The rating system developed by Assetdyne delivers, therefore, the following additional information:

Stock Complexity - this measures how "chaotic" the evolution of stock is. In other words, we're talking of an advanced measure of volatility. Complexity is measured in bits. The value of complexity of different stocks may clearly be compared.

Stock Resilience - this measures how well the stock price reacts to shocks and extreme events. Values range from 0% to 100%.

As the computation of the complexity and resilience of a stock are based on closing values at the end of each trading day, the corresponding values also change on a daily basis.

An example is illustrated below.

Assetdyne's rating system is applicable also to portfolios of stocks. The example below illustrates a small portfolio of oil&gas companies.

{kind=link}

An important aspect of this particular rating technique is that it is not based on the financial reports (Balance Sheets, Income Statements, Cash Flow, etc.) which are of highly subjective nature. But companies construct their balance statements so as to provide a more optimistic picture and therefore conventional PoD-type ratings inevitably influenced. While financial statements and the resulting PoD ratings are subjective (recall the multitude of triple-A-rated companies that have defaulted all of a sudden, triggering the current crisis) to the point that governments have sued Credit Rating Agencies, stocks represent a considerably more objective reflection of the real state of affairs. Most importantly, the information is known to everyone. Of course, markets are not always right and the price may be wrong but the process of converging to a given price is as objective and democratic as things in this world can get.

One could conclude that the World's stock markets constitute one huge social network which plays a global game called trading. As the game is played, one of its outcomes is the price of stocks. The price may be "wrong", it may be manipulated but it is what it is. It is the result of the mentioned crowd-rating and Assetdyne uses it to provide new important information on complexity and resilience rating of stocks and portfolios. Innovation in finance is possible.

www.assetdyne.com

Tuesday 17 September 2013

Complexity Introduced to Stock and Portfolio Analysis and Design

Modern Portfolio Theory (MPT) has been introduced in 1952 by Markowitz. As described in Wikipedia, "MPT is a theory of finance that attempts to maximize portfolio expected return for a given amount of portfolio risk, or equivalently minimize risk for a given level of expected return, by carefully choosing the proportions of various assets. Although MPT is widely used in practice in the financial industry and several of its creators won a Nobel memorial prize for the theory, in recent years the basic assumptions of MPT have been widely challenged by fields such as behavioral economics.

MPT is a mathematical formulation of the concept of diversification in investing, with the aim of selecting a collection of investment assets that has collectively lower risk than any individual asset. This is possible, intuitively speaking, because different types of assets often change in value in opposite ways. For example, to the extent prices in the stock market move differently from prices in the bond market, a collection of both types of assets can in theory face lower overall risk than either individually. But diversification lowers risk even if assets' returns are not negatively correlated—indeed, even if they are positively correlated.

More technically, MPT models an asset's return as a normally distributed function (or more generally as an elliptically distributed random variable), defines risk as the standard deviation of return, and models a portfolio as a weighted combination of assets, so that the return of a portfolio is the weighted combination of the assets' returns. By combining different assets whose returns are not perfectly positively correlated, MPT seeks to reduce the total variance of the portfolio return. MPT also assumes that investors are rational and markets are efficient."

Since 1952 the world has changed. It has changed even more in the past decade, when complexity and turbulence have made their permanent entry on the scene. Turbulence and complexity are not only the hallmarks of our times, they can be measured, managed and used in the design of systems, in decision-making and, of course, in asset portfolio analysis and design.

Assetdyne is the first company to have incorporated complexity into portfolio analysis and design. In fact, the company develops a system which computes the Resilience Rating of stocks and stock portfolios based on complexity measures and not based on variance or other traditional approaches. While conventional portfolio design often follows the Modern Portfolio Theory (MPT), which identifies optimal portfolios via minimization of the total portfolio variance, the technique developed by Assetdyne designs portfolios based on the minimization of portfolio complexity. The approach is based on the fact that excessively complex systems are inherently fragile. Recently concluded research confirms that this is the case also for asset portfolios.

Two examples or Resilience Rating of a single Stock are illustrated below:

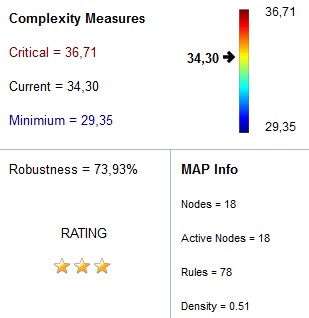

An example of a Resilience Rating of a portfolio of stocks is shown below (Top European banks are illustrated as an interacting system):

while the rating and complexity measures are the following:

The interactive map of the EU banks may be navigated on-line here.

For more information, visit Assetdyne's website.

Subscribe to:

Posts (Atom)